Last Word Cocktail & U.S. April Retail Results Show E-Commerce Continues to Take Market Share

Issue No. 9 - May 18, 2023

In today’s issue we look at the modern classic cocktail the Last Word and dig into what the U.S. April Retail results released this week by the U.S. Census Bureau reveal about E-Commerce marketshare growth and the state of the economy.

This Week’s Cocktail: The Last Word

The Last Word cocktail is both an old cocktail and a modern classic - as well as a drink with a special connection to my hometown of Seattle. The mix of gin, maraschino liqueur, green Chartreuse and lime juice was created well before Prohibition struck, but was rediscovered and embraced by bartenders and drinkers alike over the last 20 years - becoming a modern classic and spawning many a riff.

The Last Word cocktail is believed to have originated at the Detroit Athletic Club in the early 20th century, gaining some popularity through the 1920s and 1930s but eventually falling out of favor following the repeal of Prohibition in the United States. For nearly a century, the Last Word remained largely forgotten - out in the cocktail wilderness, and tucked away in the dusty annals of cocktail history.

That all changed when Murray Stenson, a legendary Seattle bartender spotted the drink in an old copy of Bottoms Up! (1951), tested it, and liked it. In 2004, Stenson put it on the menu at Seattle’s Zig Zag Cafe, where he was working at the time. The Zig Zag was a very influential bar in the early days of the cocktail renaissance, and remains a fantastic bar - just down the hillclimb from Pike Place Market on the way down the Seattle waterfront (no more Viaduct!). To this day, I regularly recommend it when I’m asked for my list of favorite Seattle bars.

After Stenson put onto the menu at the Zig Zag, the drink spread through the - at the time still nascent - cocktail community, and it was soon being served in New York and elsewhere, attaining the elite status of a '“bartender’s handshake” — that is, a cult cocktail that, when ordered, communicates you are in-the-know to all the barkeeps and booze enthusiasts within earshot.

In some ways that is still true. When I recently stopped in at the Zig Zag when a work dinner downtown moved out an hour I sauntered in and ordered one without looking at the menu. The bartender gave me a knowing nod, and the pic above is the delicious and perfectly refreshing Last Word the bartender mixed up for me on what was an unusually warm, spring evening in Seattle.

The Last Word is known for its equal parts recipe, creating a well balanced cocktail with simplicity. The gin provides a botanical backbone, the green Chartreuse adds herbal complexity, the maraschino liqueur contributes subtle sweetness, and the fresh lime juice lends a bright citrusy note. The resulting cocktail is both balanced and flavorful, with a combination of herbal, floral, and tart notes. The Last word today is of course no longer a cult cocktail, it is a modern classic that has spawned many a delicious riff, such as the Paper Plane, Final Ward, Naked & Famous and many others.

The Last Word is also largely responsible for introducing Chartreuse into many mixologists’ pallets, which has now led to Chartreuse being in short supply - and thus expensive. Turns out that the monks from the 900-year-old Carthusian order in the French Alps who make Chartreuse have decided that they are more interested in their religious practice - prayer and solitude - over expanding their business and satisfying the increased demand for green and yellow Chartreuse. Personally, I respect that, though mixologists the world over have now turned to hoarding Chartreuse as a result - myself included. But there are alternatives…

While Chartreuse is made from a well-guarded, secret formula said to include 130 herbs, plants and flowers macerated in a wine alcohol base, the dominant flavor profile is from the maceration of the tops of alpine Artemisia (commonly called wormwood), which also happens to be found in other herbal liqueurs. Dolin’s Genepy Le Chamois in particular is a good alternative that leads with wormwood. In my opinion, another great option in a Last Word is the very good Americano Bianco amaro from Seattle’s Fast Penny Spirits.

Murray Stenson's rediscovery and championing of the Last Word gave fuel to the the craft cocktail movement, and gave us a great template upon which to create. His influence and the Last Word's resurgence also helped solidify Seattle's reputation as a city with a vibrant cocktail culture and a hub for innovative mixology, which of course I am very grateful for.

The spec, serves one:

3/4 oz - Dry gin (Botanist or Tanqueray N. 10 preferred)

3/4 oz - Green Chartreuse (use Dolin Genepy Le Chamois as an alternate)

3/4 oz - Luxardo Maraschino liqueur

3/4 oz - fresh lime juice

The process:

Pour all the ingredients into a cocktail shaker, then fill with ice. Shake until very well chilled, then strain the mixture into a chilled cocktail glass. Garnish with a lime twist, if desired.

Notes:

When I make a Last Word, I often bump the gin up to 1 oz. While not the classic equal parts spec, it tends in my opinion to present a bit more balanced to my palette.

I also recommended “Double Straining” this cocktail by using a small tea strainer or wire basket in addition to the hawthorn strainer or cobbler shaker to ensure you remove all the ice chips caused by shaking the cocktail. You and your guest will enjoy it even more.

Analysis: April U.S. Retail Results Show E-Commerce Continues to Take Share - And Offers Warning Signs

The Census Bureau shared some intriguing data this week that in my opinion offers up both a bit of a warning sign on the health of the American economy, and a revealing counter-narrative to how the U.S. media is reporting on the business of retail today.

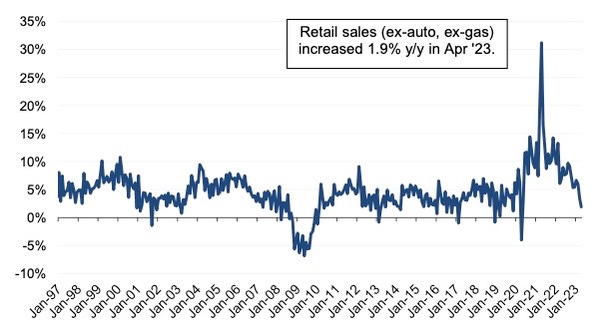

Many headlines out this week talked up the 0.4% increase in overall retail sales and the +1.9% when you exclude autos and gas in April - matching what many analysts had expected. While an improvement from March - which was down 0.5% (revised from the previously reported -0.8% decrease) - there is something in the reporting which really bothered me. What is missing from these headlines? These numbers are not inflation adjusted!

When you factor in inflation - still running close to 5% on an annualized basis - retail sales were actually down, and by quite a bit! Despite higher prices, sales are less than last year. The retail industry is already in a mild recession.

The only category in the April results showing meaningful growth is E-Commerce, which continues to take share from physical retail. The census bureau uses the odd name “Non-Store Retailer” to capture E-commerce results both from pure plays and the e-commerce and catalog businesses of omnichannel retailers - but it is plainer to simply call this e-commerce. Although growth slowed slightly, these retailers and business units still saw a 6.4% increase year-over-year in April. Year-to-date, this category has grown by 7.4%, and while that is a deceleration - from the 12.8% increase in 2022, a 15.3% increase in 2021, and a whopping 30.3% increase in 2020. E-commerce continues to take share, though the media seems obsessed with reporting on a “return to stores” narrative. This sector's continued growth suggests that online shopping is still on the rise, albeit more slowly than during the pandemic, and frankly, the media is totally missing this story in the narrative they continue to tell. “Everyone is back shopping in stores!” they say, probably because their CFOs desperately want the return of the retailers ad dollars that used to flow in to drive foot traffic. (RIP the Sunday circular, now I have nothing to start the barbecue with!)

The only category with modest growth is General Merchandise, which is benefiting from consumers trading down. Perhaps no category seems to be benefiting from both post-pandemic patterns returning and the fact that consumers are trading down than big-box general merchandisers. Although growth has slowed down a bit, General Merchandise stores still saw an increase of 4.1% year-over-year in April, following a 4.9% increase in March. So far this year, the category has risen by 5.5%. This follows gains in the past few years, with a 6.9% increase in 2022, a 9.4% increase in 2021, and a 1.9% increase in 2020. But importantly, general merch results are essentially keeping up with inflation. Every other category is flat to down.

Grocery grew, but did not keep up with inflation: Similarly, Grocery stores are also in the winners' category, despite a deceleration. In April, sales in this sector increased by 3.1% year-over-year, compared to a more robust 5.4% increase in March. Year-to-date, grocery sales have increased by 4.8%, following a 9.0% increase in 2022, a 4.3% increase in 2021, and a 9.4% increase in 2020. Despite the growth, grocery is trending slightly beyond overall inflation, but weathering the increase in both fine dining and fast-service restaurants we saw late last year and early this year just fine.

Furniture and Home Furnishings finally caught Covid: Sorry, that is a little snarky, and the reality is that these categories are being impacted by the double whammy of Covid related boom as we all nested and invested in our homes and kitchens, and the slow down in the housing market. This sector saw a significant decline, with retail sales falling 8.8% year-over-year in April. This represents a significant further deceleration from the 2.8% decrease seen in March. Year-to-date, sales in this category have dropped 1.6%, following a slight 0.5% increase in 2022, a 24.4% increase in 2021, and a 6.1% decrease in 2020.

Consumer Electronics and Appliances are lacking “it” products and are also impacted by housing slow-down: Consumer Electronics and Appliances also took a hit, with sales decreasing 8.2% year-over-year in April. This marks a decline from the 4.5% decrease in March. So far this year, the category has fallen 1.8%, following a 1.6% decrease in 2022, a 25.4% increase in 2021, and a 17.9% decrease in 2020. The same factors impacting Furniture and Home Furnishings are at play here too, as is the fact that there are no hot products or technological innovation driving consumer electronics - all that innovation is in the browser, via Generative AI.

The Building Materials, Garden Equipment, and Supplies bubble has popped: Yet another category suffering from the stalled housing market and the impact of high interest rates, this category saw a 5.7% decrease year-over-year in April, which is slightly better than the 5.8% decrease in March. Year-to-date, the category has fallen by 2.1%, following a 7.0% increase in 2022, a 14.2% increase in 2021, and a 13.1% increase in 2020.

Clothing and Clothing Accessories have the blues (and reds, and every other color - since no one is buying). Finally, Clothing and Clothing Accessories stores also experienced a decrease in April, with sales falling 4.1% year-over-year. This is a decline from the 2.0% decrease seen in March. Year-to-date, however, the category has seen a modest increase of 0.9%. But when you factor in inflation, these categories are really suffering. The fact that “return to the office” is still below 50% is certainly not helping fuel sales, and of course we are already into early spring weather in the U.S., which does not help. (It is 85% fahrenheit in the Seattle as I write this). I do expect fall and back-to-school to provide some boost in this category - I mean we will all need new clothes someday, right?

But the scary truth is that U.S. consumers are running out of gas.

Not literal gas, but “consumption gas”. Stimulus packages during the pandemic enabled many U.S. consumers to decrease their debt and stack up some modest savings - whether they were out of work or not. Many homeowners over the last decade also capitalized on lower interest rates to refinance their mortgages and take cash out of their homes, which fueled consumption.

However, now with the cessation of that pandemic stimulus, the end of the mortgage refinance boom, and the impact of higher interest rates on consumer prices, Americans are feeling the pinch. But consumption and spending have not yet markedly decreased. Instead, consumers are loading up on credit.

Total U.S. household debt rose by $148 billion, or 0.9% to a record $17.05 trillion in the first quarter of 2023, according to the latest Federal Reserve Quarterly Report on Household Debt and Credit. Mortgage balances climbed by $121 billion to $12.04 trillion at the end of March, while Auto loan balances increased to $1.56 trillion and student loans to $1.60 trillion.

Credit card balances were flat at $986 billion, but normally credit card balances typically decline in Q1 as consumers pay down holiday spending, so this is notable and concerning for the economy. Consumer spending drives nearly 70% of the U.S. economy.

And now, a growing number of Americans are struggling to keep up with payments on their consumer debt - car loans, credit cards, and mortgages - compared to the previous year. In the first quarter of 2023, the percentage of debt balances that were at least 90 days overdue rose to 1.08%, up from 0.071% a year earlier - per a report by the Federal Reserve Bank of New York.

Consumers are starting to run out of ‘consumption gas’, and that will impact the back half of the year. Perhaps this is exactly what the Federal Reserve is aiming for - the so called ‘soft landing’ - but it is going to create short term softness in the retail economy - even as e-commerce continues to take share.

ICYMI - Links of the week:

The Return to the Office Has Stalled. When average city office-occupancy rates at the start of the year surpassed 50% for the first time during the pandemic, many landlords viewed this milestone as a sign that employees were finally resuming their former work habits. Those office-usage rates have barely budged since as most companies have settled into a hybrid work strategy that shows little sign of fading. (Wall Street Journal). See also: 26 Empire State Buildings Could Fit Into New York’s Empty Office Space. That’s a Sign. (New York Times)

19 Ridiculous Tech Myths. There’s plenty of fake tech news floating around; each new generation of technology products and services begets even more false beliefs. From the skinny on 'incognito mode' to 'battery fatigue', time to get real about widely heard tech myths. (PC Magazine)

The Companies Trying to Make Live Shopping a Thing in the U.S.. Live shopping has its fans and its naysayers. Can livestreamed shopping find an audience in a crowded media & entertainment landscape? (New York Times)

TikTok’s Chinese parent has delayed the rollout of its shopping platform in the U.S.. TikTok’s Chinese parent has delayed the rollout of its shopping platform in the U.S. as concerns over the app’s future deter merchants from joining (Wall Street Journal)

Join me and meet at these upcoming events:

Bloomreach Customer Event - London - May 24th - Join us in London for a day discussing best-practices, Generative AI, and other aspects of the Bloomreach roadmap.

MACH 2 - Amsterdam - June 13-14, 2023 - Talking composable commerce and composable cocktails in one of my favorite cities in the world. Plus you can count on finding me at Pulitzer’s Bar at least once while I am there.

CommerceNext E-Commerce Growth Show - NYC - June 20-21, 2023 - From Amsterdam to New Amsterdam, talking about digital commerce growth. I’ll be speaking about driving customer engagement across all channels through personalized SMS marketing.

Bloomreach Edge Summit - Napa Valley - August 24-25, 2023. Join us in beautiful Napa Valley, CA to explore the impact Generative-AI will have on digital commerce and marketing. Get educated, discover key use-cases, and have a POV on the impact on your business and clients. If you can’t make the physical event, join us for the digital livestream.

If you are looking for me online, you can find me here, here, and here.

Be well, be safe, and here is to good business! Cheers! - Brian