An Anniversary Boulevardier & 2024 DTC Commerce Tech Business Outlook

Issue №22 - We celebrate the 1 year anniversary of the newsletter with a Boulevardier variation, 'The Chairman Approves'. Sip along as we dig into the outlook for DTC tech investment in 2024.

It has been a year since I started the newsletter, so I revisit both the first cocktail and first subject I featured in the first “real issue” back on February 3, 2023. But of course, both the cocktail and topic deserve and require a fresh look - so for the cocktail we do a variation on the Boulevardier I featured then, and of course look at the 2024 tech investment outlook - and what it means as we ramp into the year. Cheers!

Cocktail: The Chairman Approves, A wonderful Boulevardier variation

In celebrating the one year anniversary of the newsletter, it makes sense to mark the occasion by reflecting on the cocktail we featured in the first ‘real’ issue, the wonderful Boulevardier. As I wrote then, when pressed I will typically name the Boulevardier as my go-to cocktail - perfect for either before or after dinner, and easy enough to make and remember that I can teach any bartender who doesn’t know the cocktail how to make it from across the bar. “A Negroni with bourbon,” I will say, “But add another half ounce of bourbon, and maybe some orange bitters if you have them.” Done, though the truth is that a Boulevardier is much much more than a Negroni with bourbon.

The Boulevardier was invented at Harry’s New York Bar in Paris in the mid-1920’s. It was around 1924 that a group of Parisian expats formed a drinking club they called the International Bar Flies. Members had a secret handshake, and wore square ivory-colored enabled lapel pins meant to mimic sugar cubes used in their Old Fashioneds - the initials IBF and a cartoon fly were enabled in black.

Erskine Gwynne, a man about town

One of the members of the IBF was Erskine Gwynne, an American-born writer who founded a monthly magazine in Paris patterned after The New Yorker. He called it The Boulevardier, a term loosely referring to a man - ahem - about town. No doubt Erskine knew a thing or two about that. The Boulevardier magazine ran for five years between 1927 to 1932, and is now most famous for being the eponymous origin of the name of the cocktail that has gone on to become a classic.

The Boulevardier cocktail first appeared in print in the Parisian cocktail book Barflies and Cocktails, published in 1927. The cocktail does not appear in the main list of recipes, but rather within the essay called “Cocktails Round Town” contributed by Arthur Moss, Gwynne’s partner in the magazine endeavor. Moss described the barflies and their usual orders at Harry’s and then went on to say, “Now is the time for all good barflies to come to the aid of the party, since Erskine crashed it with his Boulevardier cocktail; ½ Campari, ⅓ Italian Vermouth, ⅓ Bourbon whiskey.”

While the Boulevardier did not catch on quickly - disappearing for nearly eighty years before reappearing in the 2007 March/April issue of Imbibe magazine - it is now considered a classic. And like many classic cocktails, the Boulevardier also happens to be a wonderful template upon which to riff - mezcal, rum, amari, or bitters are all fun to play with within this template - or double-splitting as we wrote about a year ago.

The Chairman Approves of this riff

And that brings us this riff Bill created, The Chairman Approves. Smoky and herbaceous - the bitter balancing the sweet - this cocktail is a wonderful winter sipper. The Chartreuse expression - Élexir Végétal de la Grande Chartreuse - pairs wonderfully with the peaty scotch, and the rich sweetness of the vermouth is balanced by the nuanced bitter of Gran Classico, a terrific Torino style bitter based on a recipe dating from the 1860s. (Gran Classico itself was featured in the Kickback Cadillac margarita way back in Issue No.8). If you like smoke, if you like complexity, if you are willing to flex your palette, give this one a try. And it comes with a secret ingredient guaranteed to make for an interesting conversation (if you are a cocktail nerd like us).

A bit about Élexir Végétal de la Grande Chartreuse - the secret to this great cocktail

Just as we see Chartreuse in short-supply, we have seen another product from the famed Carthusian monks from the Chartreuse Mountains north of Grenoble gain in distribution - and it was in fact the predecessor to the Green and Yellow Chartreuse that has gained wide popularity today.

According to lore, Élexir Végétal de la Grande Chartreuse came from a recipe entrusted to the Carthusian monks by the Duke of Estrees - François Annibal d'Estrées, Marshal of France - in 1605. It was contained in a mysterious manuscript that bore a recipe made up of 130 plants, herbs, and flowers. It was called the “elixir of long life”. For more than a century and a half, the Carthusians would further develop and refine this recipe until the final product ‘was fixed’ in 1764, and it has remained unchanged since. It was not until 1840, that the monks developed a milder version of “The Élixir” - that version is a liqueur now known as Green Chartreuse. At the same time they created an even sweeter version now marketed as Yellow Chartreuse. (We go deep here on the newsletter!)

The monks intended their élixir to be used as medicine, and Brother Charles of the Carthusian Order was the first to market it in local markets as such, descending on a donkey from the monastery into the towns and villages nearby. The elixir gained renown during the cholera crisis of 1832, and became more widely known throughout France as a result.

Today the liqueur is produced in the distillery nearby by the Grande Chartreuse monastery in Aiguenoire, France. Élexir Végétal de la Grande Chartreuse today can be thought of as a concentrated form of Chartreuse, and something you would only use a small amount of. We use it as you might use cocktail bitters or absinthe - a few dashes to add an herbaceous, wonderful twist on a cocktail.

Chartreuse was born as an “elixir of long life”, so perhaps it is fitting that it has never been more popular - five centuries on. I think the Chairman will approve.

Cheers!

I would like to acknowledge the sources used in research for this article:

“Vintage Spirits and Forgotten Cocktails” By Ted Haigh, Quarry Press, 2020

“Signature Cocktails” By Amanda Schuster, Phaidon Press, 2023

History of Chartreuse, Chartreuse website

The Chairman Approves Cocktail Spec, serves one:

2 oz (~60 ml) - Ardbeg 10 Yr Islay Single Malt Scotch Whisky (substitute any peaty single malt scotch)

1 oz (~30 ml) - Gran Classico Bitter

1 oz (~30 ml) - Cocchi de Torino Vermouth

2 dashes - Élexir Végétal de la Grande Chartreuse

Garnish - Grapefruit twist (see note)

The process:

Combine all ingredients into a cocktail pitcher. Add ice. Stir and strain into a small chilled or frozen cocktail coupe. [Preparation time: 5 minutes]

Notes:

When applying a citrus peel twist - grapefruit in this case - it is important to express the oils in the peel on the top of your cocktail - and not just drop it in. This adds aroma and another layer of complexity to your cocktail - adding a bitter, floral and sweet note to the nose. Great bartenders and mixologists also will often run the twist across the rim of the glass and even the stem of a coupe to enhance the experience of sipping and holding the drink even further.

Why do we primarily feature Total Wine & More in our links to the booze? Distribution mostly, as TW&M is America’s largest independent retailer of fine wine and spirits - with 264 stores across 28 states. They also happen to be good people and offer a great BOPIS service. C&C receives no compensation or benefit from any of our links - we don’t do affiliate shit, and if we ever do we will let you know.

The One Year Anniversary of Cocktails & Commerce - Thank you!

Thank you all. It was a year ago I started writing my newsletter, and the response has been wonderful. Cocktails & Commerce is now well on our way to 2,000 subscribers, and that is largely thanks to you. I want to thank you all for being subscribers, and the many of you who have shared C&C with others - whether that is a post on LinkedIn or through forwarding the newsletter. Our growth is because of you.

I started writing the newsletter as an experiment of sorts. Did I have something to say? Would I enjoy writing about the industry again? Could I develop an independent voice after so many years working as a marketer and a strategist within the industry? And perhaps most importantly, would people want to read it? Because of the response and what many of you have shared with me, I feel I can answer that question. So thank you again.

And the drinks? I wanted to give my readers something to enjoy in every issue, even if they were exhausted and not in the mood for my analysis - or worse, didn’t care. Sharing my enthusiasm for mixology seemed a natural fit. I said above “our newsletter” because this is indeed a collaboration. The cocktails and the research behind them is certainly where the collaboration with Bill began - he has contributed a tremendous amount of input from the start - but Bill’s perspective is also all over the analysis, with his input and critique infused throughout.

The newsletter is of course free, and we intend to keep it that way. We may add a paid subscription tier in the future - along with other content - but have no intention of changing the free nature of this newsletter. We love the privilege of landing in your inbox - and your engagement with what we have to share - and I would hate for a few bucks to stand between us.

As many of you know, we also started what we describe as a “boutique strategic advisory business” last fall - StrategyēM. The response there has been a welcome surprise, and it is another privilege for us to focus on work we love, and hopefully add value to our clients - technology and services providers both inside and outside the commerce and marketing technology space. Reach out if you ever want to learn more. (I’ll stop there, we don’t want this newsletter to sound like an advertorial!

Cheers, and thanks again, Brian

Analysis: 2024 DTC Commerce & MarTech Business Outlook

What a difference a year makes, again.

A year ago in the first edition of Cocktails & Commerce, I opened the analysis of 2023’s tech business outlook by saying, “What a difference a year makes.” The same sentiment seems relevant once again as the market has turned from sour to a more balanced set of flavors - even sweet for some. It is a good time of year to take pulse of the market and think about what we may expect - and thankfully we have some data to explore to help us make sense of the market. So let’s dig in.

2023, Recession? Ya, not so much - at least in the U.S.

Entering 2023 we were all reading the same reports and forecasts about a looming recession, expectations that consumer demand would wither in the face of inflation, money and credit would tighten, and that slowing online growth would see businesses turn conservative with their investment strategies.

But what was supposed to be a challenging year for businesses and consumers alike turned into an overall healthy business environment. Inflation came under control, wages grew, and the unemployment rate remains historically low and stable. Those with retirement savings and 401k accounts are feeling more secure. And while it can be hard to establish causality here - due-to or as-a-result-of - the American consumer surprised us all, showing resilient spending through 2023.

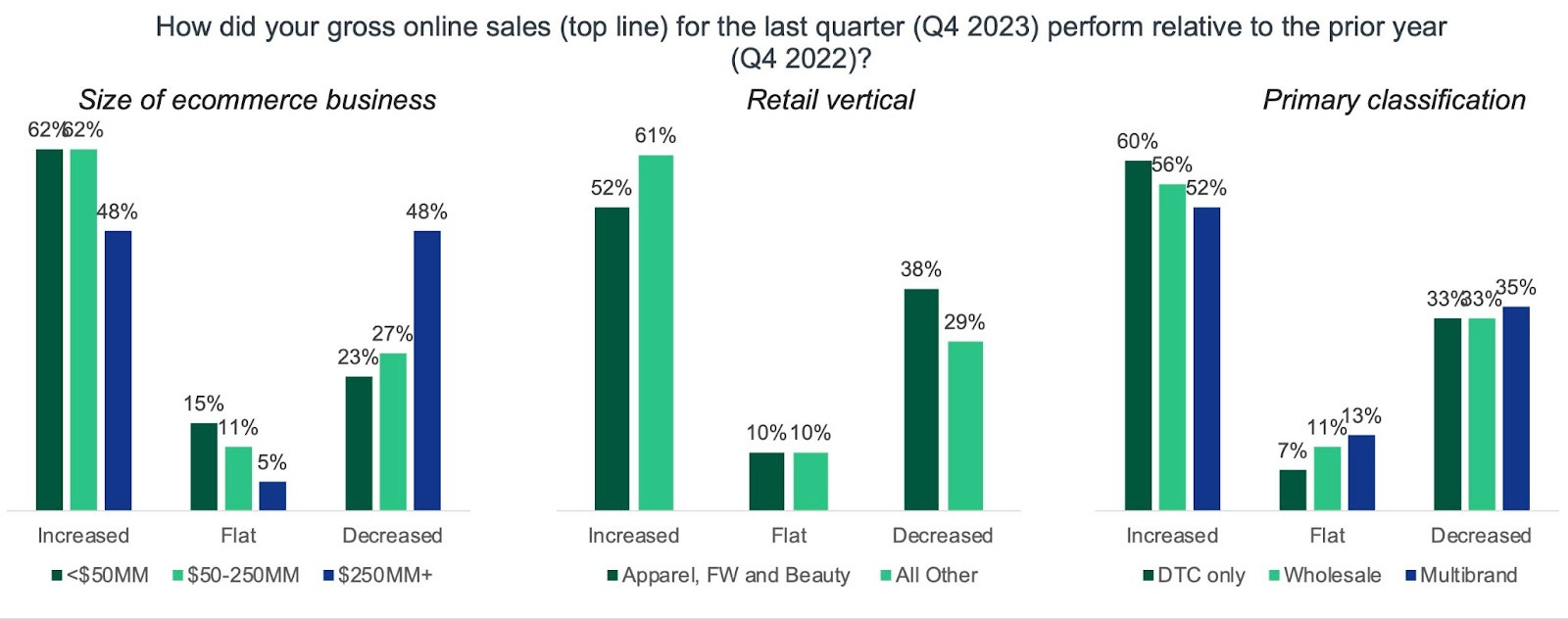

Sure, there was the well observed shift in spending to services and travel in the middle of the year - sipping amari in Turin, for example - Americans shifted with the sun to return to spending on goods once the weather changed, kids were back in school, and the holidays rolled around. The year ended strong. In Q4 2023, 56% of retailers reported growth in their business, with 29% seeing above 10% growth. (Source: CommerceNext/Forrester Retail Sentiment Survey 2024)

Interestingly, the results as 2023 ended were uneven, with small to mid-sized eCommerce businesses doing well; DTC, and categories outside Apparel, Footwear, and Beauty performing the best on year-over-year basis; and large multi-brand retailers struggling. (See chart below.)

US economy looks back on the rails, consumers are ready to ride baby!

Heading into 2024 we are hearing and feeling a much different thesis about the American economy. Investors are banking on rate cuts, big tech stocks are driving a bull market, the job market remains overall healthy, and as a result - the American consumer is growing more confident.

The U.S. Consumer Sentiment Index improved a whopping 13% in January - reaching its highest level since July 2021. And over the last two months, consumer sentiment has climbed a cumulative 29%, the largest two-month increase since a recession was wrapping up in 1991. Notably, this time we are not emerging from a recession.

And interestingly, down in data, we see that the biggest contributors to the boost in consumer confidence is a 27% surge in the short-run outlook for business conditions, and a 14% gain in consumers' views of their current personal finances. Wowza!

What all that means for tech & services investment in the U.S.

Late this past December - right around Christmas - we kept hearing a common refrain from our many conversations across the market. Deals that tech and services providers had on the table with their retail and DTC clients had been stuck in Q3 and Q4, as these clients took a wait-and-see approach to the Holiday results. They were waiting to read the tea leaves in their spreadsheets. But once the results came in - and were solid or better that expected - green-lights started going off and many tech and services firms closed meaningful business right at the end of the year. Maybe there was some of the ol’ ‘let’s use 2023 budget before it disappears’ action here too, but the sentiment was that clients' business outlook had changed, and they were ready to invest.

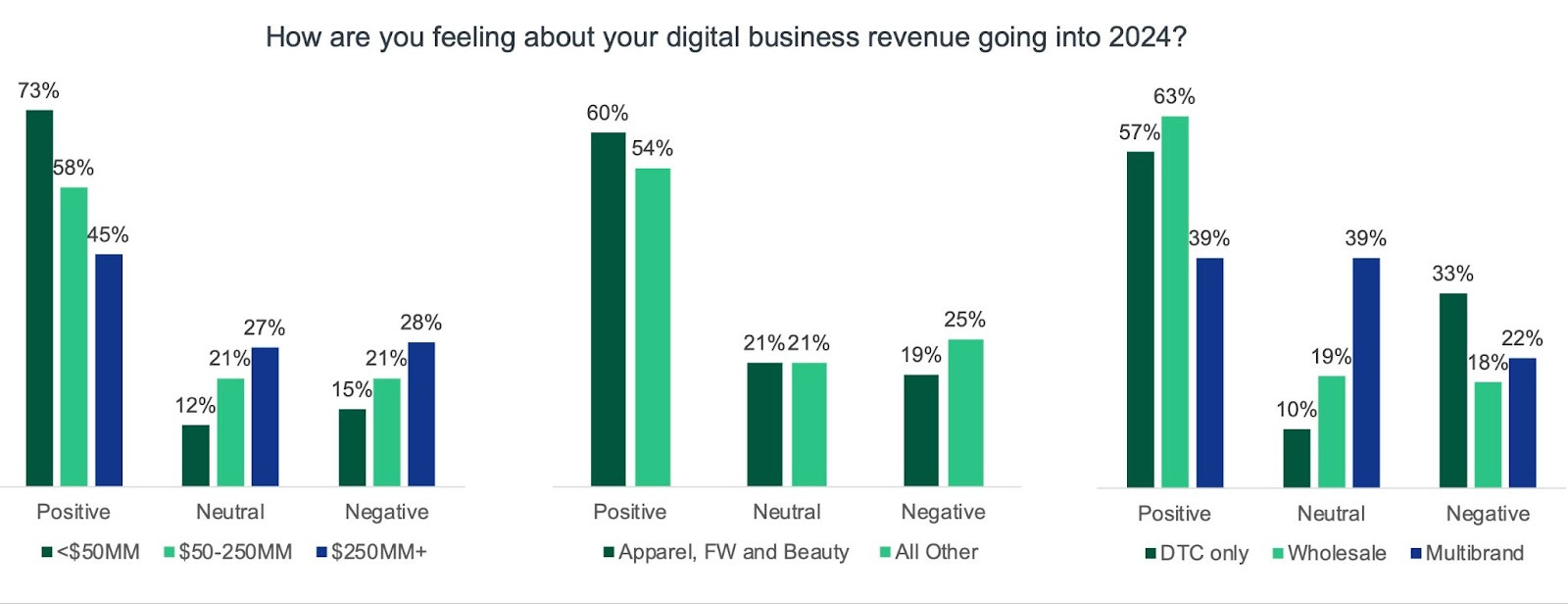

The data seems to bear that out. In part due to the strong Holiday 2023 results, a solid year overall, and a solid macro environment. Fifty seven percent of the U.S businesses CommerceNext and Forrester surveyed are feeling positive to very positive about their digital business revenue growth heading into 2024. Twenty one percent are feeling negative, and only 1% are feeling very negative. Reflecting the results above, it is small to medium sized digital businesses that are the most positive, while large multi-brand retailers are the most negative.

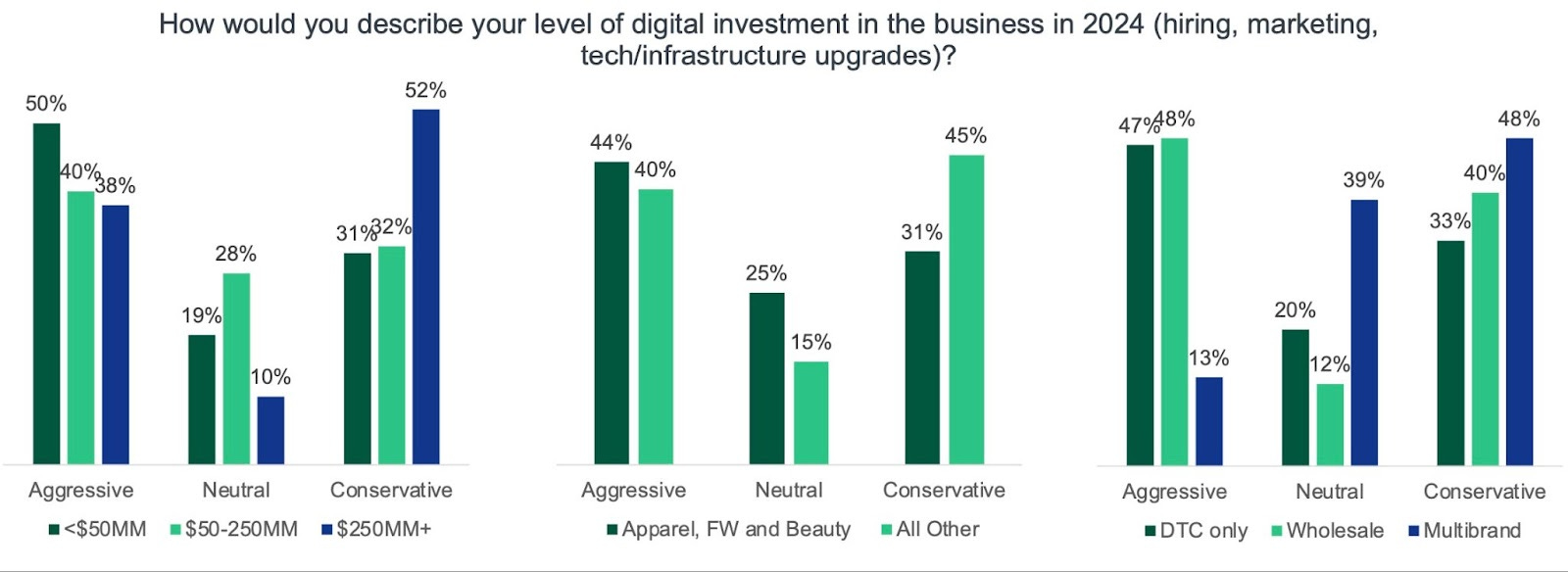

Naturally, this optimism translates into the level of investment these businesses plan to make in technology, services, people, and marketing. Forty two percent of businesses report being somewhat aggressive to very aggressive in their level of digital investment in 2024 - though to be balanced, while a concerning 39% plan to be conservative or even look to cut costs in 2024. But looking into the segmentation here, the story is more clear - again we see the tilt toward SMB and ‘mid-market’ DTC, and away from larger multi-brand retailers. (I think I may be finally picking up on a theme here.)

However, it is important to understand that the EU economy is in a far different place

The gap in economic activity between the U.S. and eurozone is widening significantly. While the U.S. economy is growing at the healthy clip of 3.3% on an annualized rate, the eurozone economy stagnated late last year as a lingering energy crisis sparked a loss of competitiveness across many European sectors, and consumers reined in spending to grapple with high living costs.

It may be surprising to hear, but economic output in the 20 countries that use the euro currency grew at zero percent in Q4 2023 versus Q3, after contracting in the third quarter. Yep, a big fat zero. And year over year, the eurozone grew by just a tenth of a percent. The Eurozone came within a hair of the definition of recession. Or to use the metric system, a millimeter. (Source: Eurostat)

Wages are also stagnant in Europe. Perhaps a decline in prices may get consumers to start spending more, but that is not good news for those marketing and selling to them. The mood in Europe is thus very different than in the U.S., and we can expect the investment levels in Europe in digital commerce and marketing tech and services to be commensurate what that mood and the reality of the broader market.

What all that means to you - the tech and services businesses serving this market

Looking at all this data, it would be easy to say - in the U.S. anyway - that, “Hey, market conditions are good. If your pipeline is not growing nicely and you are not closing deals, you have much bigger problems.” But of course the reality is much more nuanced:

Target market matters. The data is pretty clear, the action in the commerce and martech landscape is in the DTC SMB and mid-market. Larger retailers, especially multi-brand big-box or department stores have a very different perspective on 2024, and are in a much more conservative mood. SMB and Mid-market is a volume game, and tech and services companies serving - or wanting to serve - these markets will need to focus on SEO, demand-gen, improving their G2 Crowd ratings, and have a smooth, quick sales process. The good news is that you are more likely to work with a founder, CEO, or very senior-level person inside these smaller organizations, while the bad news is that many of them are not very experienced at buying software and services - and the ask to trial the software may be critical to them. And of course, the product and packaging needs to be designed differently from that which targets large enterprises in order to serve this end of the market effectively - with more holistic and all-inclusive offerings priced aggressively being more likely to do well. (Duh!)

Results will vary depending on the solution space. We unfortunately do not have data on where the temperature in the market is - in other words what solution spaces are hot or warm, or where it is reaching hypothermia - but from our market-checks evidence suggests that there are few areas that seem warm with respect to new customer investment - OMS, personalization, search/merch are three that seem to stand out from all the conversations we are having. OMS demand seems to be driven by inventory visibility and multi-nodal fulfillment (stores and drop-shippers), and personalization is complicated as the point-solution market is impacted by Gen-AI - for both good and bad. While search is not just search, but merchandising as well - particularly for the DTC mid-market that needs a better solution than they can get from their commerce platform.

And the band played on… the enterprise market is behaving differently from the past. You have of course heard this from us before - and frankly, you probably already knew it - the enterprise game has changed. The commerce and marketing tech markets in the US was a ground game led by Commerce Platforms and Content Management Systems (CMS) largely sold to IT and Email Service Platforms (ESPs) sold to marketing - everything else following. Many a point-solutions sales processes were interrupted or superseded by these large solutions and the decisions around them. Like American football, that ground game has given way to the passing game - a very different game with a similar set of rules. The advent of API-first “best-of-breed” SaaS solutions has led to composable capabilities that plug into and complement the large install bases of these larger solutions are now at the fore. The slowing replacement cycles of commerce platforms - and other large platforms - in a sense necessitate that, but it is also a fundamental change in how both IT and marketing want to buy and build software and leverage technology. As a result, point-solutions that haven’t done so already need to shift their partner strategy and GTM to more directly go after their market - complimenting the install base versus focusing on replacing it. The winners are the ones that can deploy quickly, with the least amount of risk, and which can minimize disruption to their clients' business operations and legacy technology landscape. That will no doubt shift again, with large technology transformations - such as implementing a full MACH stack, which many want to argue for - but that is not how the game is playing out - at least for now.

Stay close to your customers, who want to be more than just customers. From talking to many in the market across a range of solution areas, we keep hearing the same thing - all the growth is coming from the install base. Digital business continues to grow and mature - becoming more and more strategic for every business - and the solutions that do a good job of staying close to their customers, supporting their utilization and benefits, and of course continue evolving their solution to meet the key needs are the ones benefiting the most. This is a good thing, but it does mean that organizations have to be intentional about - and every function from sales, marketing, product, AND support have a role to play to make the “expand motion” really work. This is a muscle many solution and services providers can strengthen, and may require a shift in budget, focus, and growth hypothesis.

There remains a healthy dose of skepticism and cautiousness. While, a lot could go wrong with the US economy and consumer confidence, including the impact from a couple of awful and potentially escalating wars which could impact energy prices and supply chains - and thus a return to inflation; the Fed holding back from delivering on the markets’ baked-in expectations and causing a market reaction and a banking crisis; and a highly contentious shit-show of a presidential election cycle which may not only both distract consumers but also freak them out, regardless of their stripes. And beyond that, merchants are still cautious. The CommerceNext/Forrester report included anecdotes collected from the respondents. Despite the overall bullish data, many comments ranged from ‘Digital and tech spend continues to rise and put pressure on profitability’ to ‘After years of investment, we are taking a pause and evaluating effectiveness, efficiency and incrementality [sic]’. These reflect the sentiments of skeptical buyers. Perhaps always true, but now more than ever, the solutions they buy now have to solve specific problems with clear value attached. Claims of incredible conversion lift- or metrics not tied directly to the specific solution in question - those will only be a turn off. Vendors in this market need to sharpen up the marketing, dig into use-cases and real customer stories, and not rely on lazy claims.

I could make all the above a veiled pitch for StrategyēM’s services - or those of our many friends - but I promised you I would not do that (but maybe I just did! Ha!). But I hope the above helps you think about where your business is headed, how you will compete, and how you can be successful.

Note: Many thanks to subscriber and ‘friend of the newsletter’ Scott Silverman for pointing me to the recent data that his organization, CommerceNext, created in partnership with Forrester Research - it is greatly appreciated. What is evident from looking at it is that the research was done with one of the best analysts in our business, Sucharita (always Mulpuru to me) Kodali. This research has Sucharita’s fingerprints all over the glass (this is a cocktails newsletter, remember), and it remains an honor to call Sucharita a former colleague. Thank you to both CommerceNext and Forrester for the research and to Scott in particular for sharing it with me.

For those interested in the deck with the full research conducted by CommerceNext and Forrester, I am hosting it here with permission for you to grab if you want to have the data.

If you are looking for Brian online, you can find him here, here, and here. And find Bill here and here.

Be well, be safe, and here is to good business! Cheers!

Cocktails & Commerce™ is a wholly owned subsidiary of StrategyēM, LLC.

Another great installment. Cheers as always. Predictions are always a murky business, but I concur on the rift betwixt the U.S. and Europe. In the CMS market, for example, it's clear that many European-based platforms are looking at the addressable North American market as a key part of the strategy this year (and for some, perhaps a lifeline).

Thought I might share this "shot" of Boulevardier: I ran into a content mangaement colleague at the CMS Kickoff in St. Pete two weeks ago, and he referenced your recent use of Zombies in our conversation.

I, of course, immediately knew what he was talking about. That's viral, man.